CryptoSignalScanner - DeFib v2 indicatorDESCRIPTION:

The DeFib indicator combines Moving Averages data points, Fibonacci sequence calculations and other methods to help traders make better decisions when it comes to entering and exiting trades at different time intervals. By analyzing these data points, the indicator provides valuable insights into the market trends and helps traders determine optimal moments to enter or exit a trade. Moving Averages helps smooth out price fluctuations over a specified period, providing a clearer picture of the overall market direction. The DeFib indicator uses a mix of these averages and Fibonacci methods to increase its chances of finding good trade opportunities. Whether analyzing short-term trends or longer-term patterns, this indicator assists traders in identifying favorable entry and exit points, thereby supporting more informed and strategic trading decisions.

By using Moving Averages data points based on the Fibonacci Sequence (+ some extra calculations we don't wish to share), we incorporate a unique perspective into the analysis. It helps to identify key levels of interest, potential trend reversals, and areas where price action may align with Fibonacci retracement levels. The Fibonacci Sequence is a mathematical sequence in which each number is the sum of the two preceding numbers (e.g., 0, 1, 1, 2, 3, 5, 8, 13, 21, and so on).

As a result of this information some L1, L2, S1 and S2 labels are printed on the chart. The labels are printed when a candle has been closed. Those labels are an indication when to enter or exit a trade. How to use those labels is described in the section "HOW TO USE" below.

This indicator is versatile and can be used on any timeframe, offering a wide range of features to support traders in their decision-making process. Here are some key aspects of this indicator:

User-Friendly:

Traders can easily customize all the settings according to their preferences, ensuring a personalized trading experience.

Long Signals:

The indicator provides both normal and strong long signals, which assist traders in identifying potential reversals in the market. These signals act as confirmation for traders to consider entering a long position.

Short Signals:

Similarly, the indicator offers normal and strong short signals, helping traders identify and confirm potential market reversals for short positions.

Fibonacci Sequence Calculation:

The calculation of the Long and Short labels is based on the Fibonacci Sequence, a mathematical pattern widely used in technical analysis. This adds a reliable and systematic approach to the indicator's signal generation.

Stop Loss:

When initiating a trade, it is our standard practice to implement a stop loss order based on the stop loss signal derived from the current or preceding candle. These stop loss signals are generated using the Average True Range (ATR) indicator.

Overlays:

The indicator includes overlays that visually represent market trends. These overlays identifying support and resistance levels, and providing valuable insights into the overall market behaviour.

Trend Table Box:

Traders can access a trend table box that displays the prevailing trend across different timeframes. This feature allows traders to assess the trend's strength and consistency. Additionally, users have the flexibility to adjust the timeframes based on their trading preferences.

Long/Short Alerts:

The indicator offers the functionality to add alerts for both long and short positions. Traders can set up notifications to be alerted when specific conditions are met, ensuring they stay informed even when they're not actively monitoring the charts.

Overall, this indicator provides traders with a comprehensive set of tools and features to enhance their trading decisions. Its user-friendly nature, combined with the inclusion of various signals, overlays, trend analysis, and alerts, enables traders to make informed choices and adapt to different market conditions effectively.

HOW TO USE:

This indicator incorporates specific signals that provide valuable insights into potential trend reversals in the market. Here's how each signal type is interpreted:

L1 (Long) Signal:

When an L1 signal appears, it suggests a potential uptrend reversal. Traders should pay attention to this signal as it indicates a possible shift from a downtrend to an uptrend. It serves as an early indication of a potential upward movement in prices. This is the fist point where we can take a long position. If we want to invest $100 into this trade we invest a maximum of $50 at this point. Don't forget to put a stop loss as described below in the "STOP LOSS" section.

L2 (Long) Signal:

An L2 signal acts as confirmation of the potential uptrend reversal identified by the L1 signal. When an L2 signal emerges, it strengthens the case for an upcoming uptrend. Traders may consider this signal as a stronger indication to support their decision to enter a long position. This is the point where we can invest another $50 if we already invested on the L1 signal. If we did not invested yet and we still see a clear reversal we enter the trade here with $100. Don't forget to put a stop loss as described below in the "STOP LOSS" section.

S1 (Short) Signal:

When an S1 signal is generated, it suggests a potential downtrend reversal. Traders should take note of this signal as it indicates a possible shift from an uptrend to a downtrend. It serves as an early indication of a potential downward movement in prices. This is the fist point where we can take a short position. If we want to invest $100 into this trade we invest a maximum of $50 at this point. Don't forget to put a stop loss as described below in the "STOP LOSS" section.

S2 (Short) Signal:

An S2 signal confirms the potential downtrend reversal identified by the S1 signal. When an S2 signal emerges, it reinforces the likelihood of an upcoming downtrend. Traders may consider this signal as a stronger indication to support their decision to enter a short position. This is the point where we can invest another $50 if we already invested on the S1 signal. If we did not invested yet and we still see a clear reversal we enter the trade here with $100. Don't forget to put a stop loss as described below in the "STOP LOSS" section.

These signals provide traders with a systematic framework to identify and evaluate potential reversals in market trends. By combining the information provided by both the L1 and L2 signals (for uptrends) or the S1 and S2 signals (for downtrends), traders can gain more confidence in their assessments of trend reversals. This indicator offers traders a valuable tool to capitalize on these reversal opportunities and make more informed trading decisions.

It is important to exercise caution and avoid blindly following the signals generated by the indicator. Instead, it is recommended to seek additional confirmations from other technical indicators such as the RSI (Relative Strength Index), MACD (Moving Average Convergence Divergence), or any other indicators that you are familiar with and trust.

While the signals provided by the indicator can be a useful starting point, relying solely on them may not always guarantee accurate predictions. By considering other technical indicators, traders can gain a more comprehensive view of the market conditions and validate the signals received from the indicator.

The RSI is a popular momentum oscillator that measures the speed and change of price movements. It helps traders identify overbought and oversold conditions, giving insights into potential trend reversals. The MACD, on the other hand, combines moving averages to provide signals for trend identification, as well as momentum and divergence analysis.

By utilizing these additional indicators or any others that you are familiar with, you can confirm the signals generated by the indicator under consideration. This approach enhances the reliability of your trading decisions by adding another layer of analysis and reducing the potential for false signals.

Each trader may have their preferred set of technical indicators based on their trading style and experience. It is important to select indicators that align with your trading strategy and complement the signals received from the indicator in question. This way, you can make more informed and well-rounded trading decisions, increasing the probability of successful trades and minimizing potential risks.

Stop Loss:

When initiating a trade, it is our standard practice to implement a stop loss order based on the stop loss signal derived from the current or preceding candle. These stop loss signals are generated using the Average True Range (ATR) indicator.

By employing a stop loss order, we aim to limit potential losses in case the trade moves against our anticipated direction. The stop loss signal, determined from the current or previous candle, provides a specific level at which the stop loss order is placed.

The Average True Range indicator is utilized to gauge the volatility of the market and determine an appropriate stop loss level. It takes into account the price range of the asset over a defined period, considering both high and low price points. By using the ATR, we can identify an optimal stop loss level that accounts for the asset's recent price fluctuations.

Implementing a stop loss based on the ATR-derived signal adds a layer of risk management to our trading strategy. It helps mitigate potential losses by automatically triggering the stop loss order if the price reaches or exceeds the predetermined level. This approach allows us to protect our capital and minimize the impact of adverse price movements.

It is important to note that the ATR-based stop loss signals should be used in conjunction with other analysis techniques and indicators. They serve as a dynamic reference point that considers market volatility, ensuring the stop loss level is adjusted accordingly.

By incorporating stop loss orders based on the stop loss signals derived from the current or previous candle using the ATR indicator, we aim to safeguard our trades and manage risk effectively. However, it is important to continually monitor and adjust the stop loss level as market conditions evolve, adhering to our risk management strategy throughout the duration of the trade.

Candlestick Sequence:

The Candlestick Sequence is a calculation used to identify potential trend reversal points in the financial markets. It consists of two main components, the Candlestick Sequence and the Candlestick Reversal. The Candlestick Sequence and Candlestick Reversal offer a structured way to identify potential reversals in the market.

WARNING:

• It is not advisable to engage in Leverage Trading unless you possess chart reading skills.

• It is not advisable to engage in Leverage Trading unless you are capable of interpreting technical indicators such as RSI, Moving Average, MACD, and others.

• It is crucial not to blindly follow trading signals without conducting your own analysis (DYOR - Do Your Own Research).

• Avoid succumbing to FOMO (Fear Of Missing Out) and impulsively entering trades. If you miss an entry point, it is important to let it go and patiently wait for the next potential entry point.

Leverage trading involves trading with borrowed funds, which amplifies both potential profits and losses. To participate in this form of trading, it is imperative to possess a certain level of expertise and knowledge. One key requirement is the ability to read and analyze charts effectively. Chart reading involves understanding various chart patterns, price movements, and support and resistance levels, among other factors. Without this skill, it can be challenging to make informed decisions and manage risk appropriately.

Additionally, leverage trading relies on technical indicators to identify potential trading opportunities and gauge market conditions. It is essential to have the ability to interpret indicators such as RSI, Moving Average, MACD, and others, as they provide valuable insights into market trends, momentum, and potential reversals. Ignoring or misunderstanding these indicators can lead to incorrect trading decisions and increased risk exposure.

Moreover, it is crucial not to blindly rely solely on trading signals, including those generated by indicators or other sources. While signals can be helpful, they should always be complemented by conducting one's own analysis. This entails conducting thorough research, considering multiple factors, and validating the signals with additional indicators or technical analysis techniques. This approach helps in making more informed and well-rounded trading decisions.

Finally, FOMO can be a detrimental emotion that drives impulsive and irrational trading behavior. It is important to avoid entering trades solely because of the fear of missing out on potential profits. If an entry point is missed, it is recommended to exercise patience and discipline by waiting for the next suitable opportunity. This approach helps to avoid unnecessary risks and maintain a more strategic and calculated trading approach.

By adhering to these warnings and taking the necessary precautions, traders can approach leverage trading more responsibly and increase their chances of success while mitigating potential losses.

REMARKS:

• It is important to emphasize that any information or content you encounter here is not intended as financial advice. We want to make it clear that we are not authorized or qualified to provide personalized investment advice. Our content, including ideas, opinions, views, predictions, forecasts, commentaries, suggestions, or stock picks, should be viewed strictly as informational, entertaining, or educational material.

• We emphasize that you should not construe the information provided here as personal investment advice or as a recommendation to take specific investment actions. It is crucial to conduct your own research, consider your individual financial circumstances, and consult with a qualified financial professional before making any investment decisions.

• While we aim to provide accurate and reliable information, we cannot guarantee the absence of errors or inaccuracies. Therefore, it is recommended to independently verify any information provided and exercise your own judgment when using it for decision-making purposes.

• Please be aware that any actions you take based on the information found here are done so at your own risk. We disclaim any liability for the consequences of your actions or decisions stemming from the information presented.

• Our intention is to provide helpful information that can contribute to your overall understanding and assist you in making better-informed decisions. However, it is essential to exercise caution, seek professional advice, and take responsibility for your investment choices.

Cheers & Good luck.

חפש סקריפטים עבור "stop loss"

[LTS] Marubozu Candle StrategyOVERVIEW

The Marubozu Candle Strategy identifies and trades wickless candles (Marubozu patterns) with dynamic take-profit and stop-loss levels based on market volatility. This indicator combines traditional Japanese candlestick pattern recognition with modern volatility-adjusted risk management and includes a comprehensive performance tracking dashboard.

A Marubozu candle is a powerful continuation pattern characterized by the complete absence of wicks on one side, indicating strong directional momentum. This strategy specifically detects:

- Bullish Marubozu: Close > Open AND Low = Open (no lower wick)

- Bearish Marubozu: Close < Open AND High = Open (no upper wick)

When price returns to test these levels, the indicator generates trading signals with predefined risk-reward parameters.

CORE METHODOLOGY

Detection Logic:

The script scans each bar for Marubozu formations using precise price comparisons. When a wickless candle appears, a horizontal line extends from the opening price, marking it as a potential support (bullish) or resistance (bearish) level. These levels remain active until price touches them or until the maximum line limit is reached.

EMA Filter (Optional):

An exponential moving average filter enhances signal quality by requiring proper trend alignment. For bullish signals, price must be above the EMA when touching the level. For bearish signals, price must be below the EMA. This filter reduces counter-trend trades and improves win rates in trending markets. Users can disable this filter for range-bound conditions.

Dynamic Risk Management:

The strategy employs ATR-based (Average True Range) position sizing rather than fixed point values. This approach adapts to market volatility automatically:

- In low volatility: Tighter stops and targets

- In high volatility: Wider stops and targets proportional to market movement

Default settings use a 2:1 reward-to-risk ratio (1x ATR for take-profit, 0.5x ATR for stop-loss), but users can adjust these multipliers to match their trading style.

HOW IT WORKS

Step 1 - Pattern Detection:

On each bar, the indicator evaluates whether the candle qualifies as a Marubozu by comparing the high, low, open, and close prices. When detected, the opening price becomes the key level.

Step 2 - Level Management:

Horizontal lines extend from each Marubozu's opening price. The indicator maintains two separate arrays: one for unbroken levels (actively extending) and one for broken levels (historical reference). Users can configure how many of each type to display, preventing chart clutter while maintaining relevant context.

Step 3 - Signal Generation:

When price returns to touch a Marubozu level, the indicator evaluates the EMA filter condition. If the filter passes (or is disabled), the script draws TP/SL boxes showing the expected profit and loss zones based on current ATR values.

Step 4 - Trade Tracking:

Each valid signal enters the tracking system, which monitors subsequent price action to determine outcomes. The script identifies whether the take-profit or stop-loss was hit first (discarding trades where both trigger on the same candle to avoid ambiguous results).

PERFORMANCE DASHBOARD

The integrated dashboard provides real-time strategy analytics to automatically convert results to dollar values for any instrument:

Tracked Metrics:

- Total Trades: Complete count of closed positions

- Wins/Losses: Individual counts with color coding

- Win Rate: Success percentage with dynamic color (green >= 50%, red < 50%)

- Total P&L: Cumulative profit/loss in dollars

- Avg Win: Mean dollar amount per winning trade

- Avg Loss: Mean dollar amount per losing trade

NOTE: The dollar values shown in the dashboard are for trading only a single share/contract/etc. You will need to manually multiply those numbers by the amount of shares/contracts you are trading to get a true value.

The dollar conversion works automatically across all markets:

- Futures contracts (ES, NQ, CL, etc.) use their contract specifications

- Forex pairs use standard lot calculations

- Stocks and crypto use their respective point values

This eliminates manual calculation and provides immediate performance feedback in meaningful currency terms.

CUSTOMIZATION OPTIONS

ATR Settings:

- ATR Period: Lookback length for volatility calculation (default: 14)

- TP Multiplier: Take-profit distance as multiple of ATR (default: 3.0)

- SL Multiplier: Stop-loss distance as multiple of ATR (default: 1.5)

EMA Settings:

- EMA Length: Period for trend filter calculation (default: 9)

- Use EMA Filter: Toggle trend confirmation requirement (default: enabled)

Visual Settings:

- Bullish Color: Color for long signals and wins (default: green)

- Bearish Color: Color for short signals and losses (default: red)

- EMA Color: Color for trend filter line (default: orange)

- Line Width: Thickness of Marubozu level lines (1-5, default: 2)

- EMA Width: Thickness of EMA line (1-5, default: 2)

Line Management:

- Max Unbroken Lines: Limit for active extending lines (default: 10)

- Max Broken Lines: Limit for historical touched lines (default: 5)

Dashboard Settings:

- Show Dashboard: Toggle performance display on/off

- Dashboard Position: Corner placement (4 options)

- Dashboard Size: Text size selection (Tiny/Small/Normal/Large)

HOW TO USE

1. Add the indicator to your chart

2. Adjust ATR multipliers based on your risk tolerance (higher values = more conservative)

3. Configure the EMA filter based on market conditions (enable for trending, disable for ranging)

4. Set line limits to match your visual preference and chart timeframe

5. Monitor the dashboard to track strategy performance in real-time

6. Use the TP/SL boxes as reference levels for manual trades or automation

Best Practices:

- Enable EMA filter in strongly trending markets

- Disable EMA filter if you want more trade signals but at lower quality

- Increase ATR multipliers in highly volatile markets

- Decrease ATR multipliers for tighter, more frequent trades

- Review avg win/loss ratio to ensure positive expectancy

UNIQUE FEATURES

Unlike basic Marubozu detectors, this strategy provides:

1. Automatic level tracking with memory management

2. Volatility-adjusted risk parameters instead of fixed values

3. Optional trend confirmation via EMA filter

4. Real-time performance analytics with automatic dollar conversion

5. Separate tracking of wins/losses with individual averages

6. Configurable visual display to prevent chart clutter

7. Complete transparency with all logic visible in open-source code

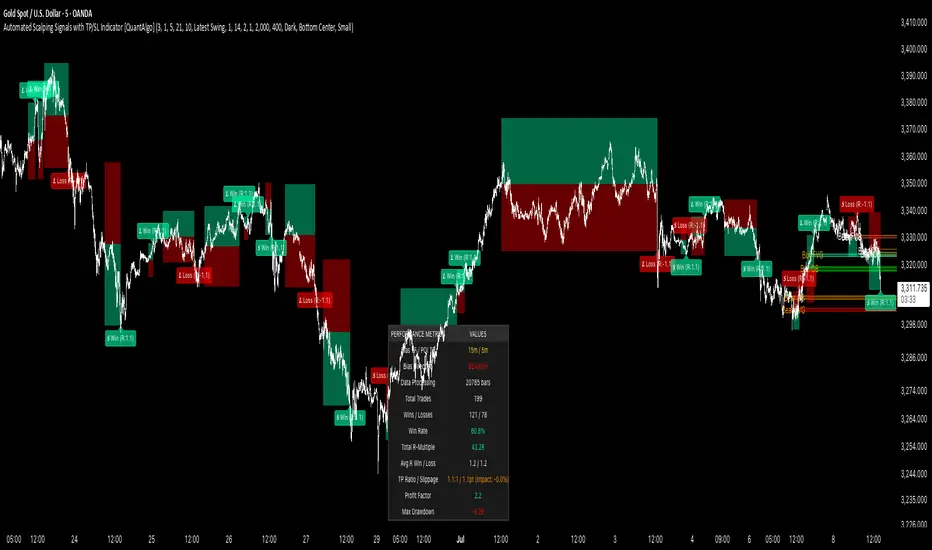

Automated Scalping Signals with TP/SL Indicator [QuantAlgo]🟢 Overview

The Automated Scalping Signals with Take Profit & Stop Loss Indicator is a multi-timeframe trading system that combines market structure analysis with directional bias filtering to identify potential scalping opportunities. It detects Points of Interest (POI) including Fair Value Gaps (FVG) and Order Blocks (OB) while cross-referencing entries with higher timeframe exponential moving average positioning to create systematic entry conditions.

The indicator features adaptive timeframe calculations that automatically scale analysis periods based on your chart timeframe, maintaining consistent analytical relationships across different trading sessions. It provides integrated trade management with stop loss calculation methods, configurable risk-reward ratios, and real-time performance tracking through dashboard displays showing trade statistics, bias direction, and active position status.

This advanced system is designed for low timeframe trading, typically performing optimally on 1 to 15-minute charts across popular instruments such as OANDA:XAUUSD , CME_MINI:MES1! , CME_MINI:ES1! , CME_MINI:MNQ1! , CBOT_MINI:YM1! , CBOT_MINI:MYM1! , BYBIT:BTCUSDT.P , BYBIT:ETHUSDT.P , or any asset and timeframe of your preference.

🟢 How It Works

The indicator operates using a dual-timeframe mathematical framework where higher timeframe exponential moving averages establish directional bias through cross-over analysis, while simultaneously scanning for specific market structure patterns on the POI timeframe. The timeframe calculation engine uses multiplication factors to determine analysis periods, ensuring the bias timeframe provides trend context while the POI timeframe captures structural formations.

The structural analysis begins with FVG detection, which systematically scans price action to identify imbalances where gaps exist between consecutive candle ranges with no overlapping wicks. When such gaps are detected, the algorithm measures their size against minimum thresholds to filter out insignificant formations. Concurrently, OB recognition analyzes three-candle sequences, examining specific open/close relationships that indicate potential institutional accumulation zones. Once these structural patterns are identified, the algorithm cross-references them against the higher timeframe bias direction, creating a validation filter that only permits entries aligned with the prevailing EMA cross-over state. When price subsequently intersects these validated POI zones, entry signals generate with the system calculating entry levels at zone midpoints, then applying the selected stop loss methodology combined with the configured risk-reward ratio to determine take profit placement.

To mirror realistic trading conditions, the indicator incorporates configurable slippage calculations that account for execution differences between intended and actual fill prices. When trades reach their take profit or stop loss levels, the algorithm applies slippage adjustments that worsen the exit prices in a conservative manner - reducing take profit fills and increasing stop loss impact. This approach ensures backtesting results reflect more realistic performance expectations by accounting for spread costs, market volatility during execution, and liquidity constraints that occur in live trading environments.

It also has a performance dashboard that continuously tracks and displays comprehensive trading metrics:

1/ Bias TF / POI TF: Displays the calculated timeframes used for bias analysis and POI detection, showing the actual periods (e.g., "15m / 5m") that result from the multiplier settings to confirm proper adaptive timeframe selection

2/ Bias Direction: Shows current market trend assessment (Bullish, Bearish, or Sideways) derived from EMA cross-over analysis to indicate which trade directions align with prevailing momentum

3/ Data Processing: Indicates how many price bars have been analyzed by the system, helping users verify if complete historical data has been processed for comprehensive strategy validation

4/ Total Trades: Displays the cumulative number of completed trades plus any active positions, providing volume assessment for statistical significance of other metrics

5/ Wins/Losses: Shows the raw count of profitable versus unprofitable trades, offering immediate insight into strategy effectiveness frequency

6/ Win Rate: Reveals the percentage of successful trades, where values above 50% generally indicate effective entry timing and values below suggest strategy refinement needs

7/ Total R-Multiple: Displays cumulative risk-reward performance across all trades, with positive values demonstrating profitable system operation and negative values indicating net losses requiring analysis

8/ Average R Win/Loss: Shows average risk-reward ratios for winning and losing trades separately, where winning averages approaching the configured take profit ratio indicate minimal slippage impact while losing averages near -1.0 suggest effective stop loss execution

9/ TP Ratio / Slippage: Displays the configured take profit ratio and slippage settings with calculated performance impact, showing how execution costs affect actual versus theoretical returns

10/ Profit Factor: Calculates the ratio of total winning amounts to total losing amounts, where values above 1.5 suggest robust profitability, values between 1.0-1.5 indicate modest success, and values below 1.0 show net losses

11/ Maximum Drawdown: Tracks the largest peak-to-trough decline in R-multiple terms, with smaller negative values indicating better capital preservation and risk control during losing streaks

🟢 How to Use

Start by applying the indicator to your chart and observe its performance across different market conditions to understand how it identifies bias direction and POI formations. Then navigate to the settings panel to configure the Bias Timeframe Multiplier for trend context sensitivity and POI Timeframe Multiplier for structural analysis frequency according to your trading preference and objectives.

Next, fine-tune the EMA periods in Bias Settings to control trend detection sensitivity and select your preferred POI types based on your analytical preference. Proceed to configure your Risk Management approach by selecting from the available stop loss calculation methods and setting the Take Profit ratio that aligns with your risk tolerance and profit objectives. Complete the setup by customizing Display Settings to control table visibility and trade visualization elements, adjusting UI positioning and colors for optimal chart readability, then activate Alert Conditions for automated notifications on trade entries, exits, and bias direction changes to support systematic trade management.

🟢 Examples

OANDA:XAUUSD

CME_MINI:MES1!

CME_MINI:ES1!

CME_MINI:MNQ1!

CBOT_MINI:YM1!

BYBIT:BTCUSDT.P

BINANCE:SOLUSD

*Disclaimer: Past performance is not indicative of future results. None of our statements, claims, or signals from our indicators are intended to be financial advice. All trading involves substantial risk of loss, not just upside potential. Users are highly recommended to carefully consider their financial situation and risk tolerance before trading.

True Market Structure [Advanced Liquidity Hunter] v1True Market Structure v1

📌 Table of Contents

1. Introduction

2. Core Concepts

3. Indicator Components

4. Configuration

5. Signal Interpretation

6. Trading Strategies

7. Risk Management

8. FAQ

________________________________________

🎯 Introduction

What is True Market Structure?

True Market Structure is an advanced technical analysis indicator that reveals hidden market mechanisms. Based on Smart Money Concepts (SMC) and ICT (Inner Circle Trader) methodology, it identifies where large financial institutions hunt retail traders' stop losses.

Who is this indicator for?

• ✅ Beginners - Intuitive visualizations and clear signals

• ✅ Intermediate - Deeper market structure analysis

• ✅ Advanced - Full parameter control and advanced strategies

Key Benefits

• 🔍 Sees the invisible - Hidden liquidity levels

• 🎯 Precise signals - Based on real data

• ⚡ Real-time - Instant analysis

• 🛡️ Capital protection - Warns against traps

💡 Pro Tip: Start with 15M timeframe! That's where most action happens - stop hunts every few candles, retail traps, liquidity battles. It's the best "microscope" to understand how the market really works.

________________________________________

📚 Core Concepts

Smart Money vs Retail Money

Smart Money:

• Banks, hedge funds, large institutions

• Create market moves, don't follow them

• Exploit retail predictability

Retail Money:

• Individual traders

• Often act emotionally

• Place stop losses at predictable levels

Liquidity

Liquidity refers to areas where many orders are waiting:

• Stop losses above highs (shorts)

• Stop losses below lows (longs)

• Orders at round numbers

Key principle: Smart Money needs liquidity to enter/exit large positions. That's why they "hunt" stop losses first, then make the real move.

________________________________________

🔧 Indicator Components

1. 💧 Liquidity Pools

What is it?

• Price levels tested multiple times

• Stop loss accumulation areas

• Displayed as blue horizontal lines

How to read?

• LIQ HIGH x15 = Level tested 15 times from above

• LIQ LOW x8 = Level tested 8 times from below

• Higher number = stronger zone

Significance:

• Price magnet

• High probability of reaction

• Smart Money target

2. 🎣 Stop Hunts

What is it?

• Candles with long wicks

• Brief penetrations of important levels

• Marked with purple labels

Types:

• STOP HUNT ⬆ - Upward hunt (shorts' stop losses)

• STOP HUNT ⬇ - Downward hunt (longs' stop losses)

Characteristics:

• Long wick (minimum 2x larger than body)

• Wick must also be larger than 0.5 ATR (default)

• Breaks recent high/low from lookback period

• Quick price return

3. 🪤 Trapped Traders

What is it?

• Areas where retail got trapped

• Failed breakouts that didn't hold

• Colored rectangles on chart

Trap types:

• 🔴 TRAPPED LONGS - Buyers caught at top

• 🟢 TRAPPED SHORTS - Sellers caught at bottom

Mechanism:

1. Important level break

2. Retail enters breakout direction

3. Price returns leaving them at loss

4. Stop losses get activated

4. 🎪 Inducement Levels

What is it?

• "Too obvious" support/resistance

• Levels respected minimum 3 times

• Orange dashed lines

Why is it a trap?

• Look like perfect trading spots

• Attract retail traders' attention

• Smart Money uses them to collect liquidity

Example:

• 100,000 level on BTC - round number

• 3 bounces = "strong support"

• Retail buys, Smart Money sells to them

5. ⏰ Kill Zones

What is it?

• Highest Smart Money activity periods

• Red background on chart

• Maximum manipulation time

Default Kill Zones:

• 🌆 London Open (08:00-09:00 UTC)

• 🏙️ NY Open (13:00-14:00 UTC)

• 🌃 Midnight (00:00-01:00 UTC)

Trading Sessions (chart background):

• 🌏 Asian (00:00-08:00 UTC) - Gray background

• 🇬🇧 London (08:00-16:00 UTC) - Blue background

• 🇺🇸 New York (13:00-21:00 UTC) - Orange background

Note: London and New York sessions overlap (13:00-16:00 UTC) - this is the highest liquidity period!

6. 🎯 Smart Money Signals

What is it?

• Potential institutional entry points

• Large labels with 🎯 emoji

• Appear after stop hunts

Conditions:

1. Stop hunt in one direction

2. High volume (2x average)

3. In Kill Zone

4. Direction reversal

7. 📊 Market Analysis Table

The table displays 9 rows with key information:

1. Session - Current trading session (ASIA/LONDON/NEW YORK/CLOSED)

2. Kill Zone - Zone status (🔴 ACTIVE / ✅ SAFE)

3. Liquidity Pools - Number of liquidity zones found

4. Inducement Levels - Number of bait levels

5. Traps (50 bars) - Number of traps in last 50 bars

6. Market Bias - Market direction:

o BULLISH 📈 (close > SMA50 and EMA21)

o BEARISH 📉 (close < SMA50 and EMA21)

o NEUTRAL ➡️ (other cases)

7. Volume - Volume status:

o 🔥 EXTREME (>2x average)

o ⬆️ HIGH (>1.5x average)

o NORMAL (>average)

o ⬇️ LOW (3 traps)

o ⚠️ CHOPPY (>5 traps)

o 👀 WATCH LIQUIDITY (>3 liquidity zones)

o ✓ NORMAL (other)

________________________________________

⚙️ Configuration

Step 1: Basic Configuration

Where to find settings:

• Method 1: Click the ⚙️ (gear) icon next to indicator name on chart

• Method 2: Double-click any indicator line/label

• Method 3: Right-click → "Settings" on indicator name

🌍 Timezone Setting

UTC Offset: Your timezone

Examples:

- London: 0 (winter) or +1 (summer)

- New York: -5 (winter) or -4 (summer)

- Tokyo: +9

🎚️ Sensitivity Adjustment

For beginners - Default settings:

• Lookback Period: 30

• Detection Sensitivity: 0.3

• Min. Touches: 2

For different timeframes:

• 15M: Sensitivity 0.2-0.3, Lookback 20-30

• 1H: Sensitivity 0.3-0.4, Lookback 30-40

• 4H: Sensitivity 0.4-0.5, Lookback 40-50

For different instruments:

• Forex Majors (EUR/USD): Sensitivity 0.1-0.2

• Indices (S&P500;): Sensitivity 0.2-0.4

• Crypto (BTC): Sensitivity 0.4-0.8

• Stocks: Sensitivity 0.3-0.5

Step 2: Advanced Configuration

🔧 Liquidity Zones Parameters

• Min. Touches (1-5): Less = more signals

• Lookback (20-200): More = further levels

• Max Zones (1-10): Display quantity control

🎣 Stop Hunt Parameters

• Wick/Body Ratio (1-5): Lower = more signals

• Min. Wick Size (0.1-2 ATR): Filters small wicks

🎯 Smart Money Analysis

• Require Kill Zone: Enable for fewer signals

• Volume Multiplier: Higher = only big moves

________________________________________

📖 Signal Interpretation

Note: Most examples are shown on 15M timeframe, because that's where you can best see all market manipulations in action!

Signal Importance Hierarchy

1. 🎯 Smart Money Signal - Strongest signal

2. 🪤 Trapped Traders - High reliability

3. 🎣 Stop Hunt - Medium reliability

4. 💧 Liquidity Touch - Needs confirmation

Interpretation Examples

Scenario 1: "Liquidity Grab"

You see: LIQ HIGH x20 at 100,000

+ Stop Hunt ⬆

+ Volume spike

= Likely decline

Scenario 2: "Trap and Reverse"

You see: TRAPPED LONGS

+ Kill Zone Active

+ SM SHORT 🎯

= Strong short signal

Scenario 3: "Inducement Break"

You see: Inducement Level break

+ No volume

+ Status: NORMAL

= Likely trap, wait

Colors and Their Meaning

• 🔵 Blue - Liquidity (neutral)

• 🟠 Orange - Caution, possible trap

• 🔴 Red - Negative signal / long trap

• 🟢 Green - Positive signal / short trap

• 🟣 Purple - Stop hunt (neutral, wait for reaction)

________________________________________

💡 Trading Strategies

Strategy 1: "Liquidity Sweep" (For Beginners)

Assumptions:

• Trade only with trend

• Wait for liquidity collection

• Enter on return

Best timeframe for learning: 15M - you'll see all manipulation stages in real-time!

Steps:

1. Identify trend (Market Bias in table)

2. Find nearest liquidity zone aligned with trend

3. Wait for price to touch and bounce

4. Enter after confirming candle

5. Stop loss beyond liquidity zone

6. Take profit at next zone

Example:

• Trend: BULLISH

• Liquidity at 100,000 (support)

• Price drops to 99,950 (stop hunt)

• Returns above 100,000

• LONG with SL 99,900, TP 101,000

Strategy 2: "Kill Zone Hunter" (Intermediate)

Assumptions:

• Trade only in Kill Zones

• Exploit stop hunts

• Aggressive entries

Ideal timeframe: 15M - in Kill Zones on 15M you'll see exactly every Smart Money move!

Steps:

1. Wait for Kill Zone (red background)

2. Watch first 15-30 minutes

3. Look for stop hunt

4. Enter immediately after stop hunt

5. Tight stop loss (0.5 ATR)

6. Scale position with profit

Tips:

• London Open - often stop hunt down, then rise

• NY Open - often tests Asian High/Low

• Midnight - position resets, false moves

Strategy 3: "Smart Money Follow" (Advanced)

Assumptions:

• Ignore minor signals

• Wait only for SM signals

• Larger positions, fewer trades

Steps:

1. Status must show HIGH RISK or WATCH LIQUIDITY

2. Wait for stop hunt series (minimum 2)

3. Watch Trapped Traders

4. Enter only on SM signal 🎯

5. Stop loss beyond last extreme

6. Hold position until opposite SM signal

Position Management:

• 1/3 position at signal

• 1/3 after direction confirmation

• 1/3 after breaking last high/low

________________________________________

🛡️ Risk Management

Basic Rules

1. Never place stop loss at obvious level

o Add 5-10 pips buffer

o Avoid round numbers

o Check where Liquidity Pools are

2. Reduce position in Kill Zones

o 50% of normal size

o Or wait until they end

3. Avoid trading at HIGH RISK status

o Unless experienced

o Then reverse logic - look for traps

Stop Loss - Where to Place?

❌ Bad places:

• Exactly below/above candle

• At Inducement Levels

• At round numbers

• Where Liquidity Pools visible

✅ Good places:

• Beyond last stop hunt

• Behind Trapped Traders zone

• Minimum 1.5 ATR from entry

• Where SM would lose significantly

Position Sizing

Safe position formula:

Risk per trade = 1-2% of capital

Position size = Risk / (Stop Loss in pips × Pip value)

Modifiers:

• Kill Zone active: × 0.5

• After SM signal: × 1.5

• HIGH RISK status: × 0.3

• With trend: × 1.2

________________________________________

❓ FAQ

General Questions

Q: Indicator shows nothing, what to do? A: Check in settings:

1. Reduce "Min. Touches" to 1

2. Increase "Detection Sensitivity"

3. Enable "Debug Mode" to see statistics

4. Ensure proper timeframe (15M+)

5. On 15M sometimes wait a few candles for first signal

Tip for 15M: If you don't see signals on 15M, enable Debug Mode. If it shows Liq=0, reduce "Min. Touches" to 1 and increase "Liquidity Lookback" to 100.

Q: Too many signals, I'm lost A:

1. Increase requirements (min. touches, respects)

2. Disable some components

3. Trade only strongest signals (SM 🎯)

Q: Which timeframe is best? A:

• 15M - PERFECT FOR LEARNING! Many signals, shows all manipulations, great for beginners

• 30M - Good balance, less noise than 15M

• 1H - Medium-term trading, clear setups

• 4H - Fewer signals but bigger moves, for patient traders

• 1D - Only major levels, position trading

💡 For beginners: Start with 15M! That's where you'll see how the market really works - stop hunts, traps, false breakouts. Only after understanding the mechanics, move to higher timeframes.

Technical Questions

Q: What does "x15" mean at LIQ? A: Number of level touches. Higher = stronger level.

Q: Why are Kill Zones red? A: High risk periods - most manipulation.

Q: What does Debug Mode show? A: When "Show Debug Info" is enabled, a label appears above the last candle with:

• Liq=X - number of Liquidity Pools found

• Ind=X - number of Inducement Levels found

• HighLvl=X - number of highs stored in memory

• LowLvl=X - number of lows stored in memory

This helps understand why sometimes no signals appear (e.g., when Liq=0).

Trading Questions

Q: Can I use only this indicator? A: Yes, but better combined with:

• Trend analysis

• Support/resistance

• Volume

Q: Does it work on all markets? A: Best on liquid ones:

• ✅ Major Forex pairs

• ✅ Main indices

• ✅ BTC, ETH

• ⚠️ Less liquid altcoins

• ❌ Exotic pairs, small caps

Q: How to remove indicator from chart? A:

• Method 1: Click X next to indicator name

• Method 2: Right-click on name → "Remove"

• Method 3: In indicators panel (left side) find and click trash icon

Q: Can I use multiple copies of the indicator? A: Yes! You can add the indicator multiple times with different settings (e.g., one for liquidity, another for stop hunts only).

Q: How much can I earn? A: Indicator doesn't guarantee profit. It's an analysis tool, not a trading system. Your results depend on:

• Discipline

• Risk management

• Experience

• Market conditions

________________________________________

🎯 Quick Start - Checklist

Pro Tip: After adding the indicator, click the star ⭐ to add to favorites - you'll have quick access in the future!

For Beginners:

• After adding indicator, set your UTC offset in settings

• Start on 15M timeframe (where you'll see the most action!)

• Observe for a week without trading

• Learn to recognize each signal type

• Practice on 15M, then try 1H

• Start with "Liquidity Sweep" strategy

• Max 1% risk per trade

• Keep trading journal

First Steps:

1. Days 1-3: Observe and learn signals

2. Days 4-7: Mark potential entries (no trading)

3. Week 2: Demo trading with small positions

4. Week 3+: Real trading with strict risk management

________________________________________

💬 Support

• Questions & Suggestions: Comments section under the indicator

• Bug Reports: Describe issue in comments with timeframe and instrument

• Updates: Click "Follow" to receive notifications

• Examples: Regular trading idea publications with usage examples

💡 Community: Share your setups in comments - let's help each other!

________________________________________

⚖️ Disclaimer

This indicator is an educational and analytical tool. It does not constitute investment advice. Trading involves risk of capital loss. Always conduct your own analysis and apply appropriate risk management. Historical results do not guarantee future profits.

GKD-C QQE of Variety RSI [Loxx]Giga Kaleidoscope GKD-C QQE of Variety RSI is a Confirmation module included in Loxx's "Giga Kaleidoscope Modularized Trading System".

█ GKD-C QQE of Variety RSI

QQE: A Comprehensive Alternative to the Relative Strength Index

The Relative Strength Index (RSI) is a popular technical indicator that measures the speed and change of price movements to help traders identify potential trend reversals, overbought, and oversold conditions. Although the RSI is widely used, it has its limitations, and traders often seek alternative or complementary indicators to improve their market analysis. One such alternative is the Qualitative Quantitative Estimation (QQE) indicator, a comprehensive oscillator that combines the features of the RSI with additional smoothing and volatility adjustments. In the following, we will explore the QQE indicator, its calculation, and its potential benefits compared to using any type of RSI alone.

QQE Indicator

The QQE indicator was developed by an unknown author and is based on the RSI with additional modifications to enhance its performance. The QQE calculation involves three main steps:

1. The first step is to compute the RSI value for a specified period using the traditional RSI formula.

2. The second step is to apply a smoothing technique, such as the Wilder's smoothing or an exponential moving average (EMA), to the RSI value, resulting in the smoothed RSI.

3. The third step is to calculate the volatility-adjusted upper and lower bands (referred to as the QQE lines) around the smoothed RSI using an ATR-based (Average True Range) multiplier.

The QQE indicator is typically displayed as an oscillator with the smoothed RSI line in the middle and the upper and lower QQE lines acting as dynamic boundaries.

Comparison with the RSI

To better understand the potential benefits of the QQE indicator compared to using any type of RSI alone, let's examine its key features and how they may contribute to improved market analysis.

Advantages

1. The QQE indicator provides a more comprehensive view of the market by combining the strengths of the RSI with additional smoothing and volatility adjustments. This may result in a more reliable and accurate reflection of market conditions and price trends.

2. The smoothed RSI line in the QQE oscillator can help filter out noise and reduce the number of false signals often experienced when using the traditional RSI alone, making it easier for traders to identify genuine trend reversals and trading opportunities.

3. The dynamic QQE lines offer an additional layer of information by accounting for market volatility. This can help traders to better gauge the strength of price movements and identify potential support and resistance levels.

4. The QQE indicator can be used as a standalone tool or in combination with other technical indicators, providing traders with greater flexibility in their market analysis.

Disadvantages

1. The QQE indicator may be more complex to understand and implement than the traditional RSI due to the additional smoothing and volatility adjustments involved in its calculation.

2. As the QQE indicator is less widely known and used than the RSI, traders may find it more challenging to find resources and support for incorporating this indicator into their trading strategies.

Conclusion:

The QQE indicator is a versatile and comprehensive alternative to the traditional RSI, offering potential benefits in terms of noise reduction, volatility adjustment, and improved market analysis. However, it is important to recognize its limitations, such as increased complexity and limited resources compared to the RSI. Traders should carefully consider the potential advantages and drawbacks of using the QQE indicator before integrating it into their trading strategies. Ultimately, the choice between the QQE and any type of RSI will depend on individual traders' preferences and the specific market conditions they are analyzing.

This indicator includes 3 types of signals

1. Middle cross

2. Levels cross

3. Slow Trend cross

This indicator includes 9 types of RSI

1. Regular RSI

2. Slow RSI

3. Ehlers Smoothed RSI

4. Cutler's RSI or Rapid RSI

5. RSI T3

6. RSI DEMA

7. Harris' RSI

8. RSI TEMA

9. Jurik RSX

Regular RSI

The Relative Strength Index (RSI) is a widely used technical indicator in the field of financial market analysis. Developed by J. Welles Wilder Jr. in 1978, the RSI is a momentum oscillator that measures the speed and change of price movements. It helps traders identify potential trend reversals, overbought, and oversold conditions in a market.

The RSI is calculated based on the average gains and losses of an asset over a specified period, typically 14 days. The formula for calculating the RSI is as follows:

RSI = 100 - (100 / (1 + RS))

Where:

RS (Relative Strength) = Average gain over the specified period / Average loss over the specified period

The RSI ranges from 0 to 100, with values above 70 generally considered overbought (potentially indicating that the asset is overvalued and may experience a price decline) and values below 30 considered oversold (potentially indicating that the asset is undervalued and may experience a price increase).

Slow RSI

The Slow RSI is a variation of the standard RSI, which introduces a smoothing technique to the RSI calculation itself. The primary difference between the Slow RSI and the standard RSI lies in the calculation of the RSI value. In the Slow RSI, the current RSI value is calculated as a moving average of the previous RSI value and the standard RSI value for the current period.

The primary advantage of the Slow RSI is that it offers enhanced signal stability, reducing noise and potentially providing more reliable trading signals for traders.

Comparison with the original RSI

To better understand the potential advantages and disadvantages of the Slow RSI, it is essential to compare its performance against the original RSI.

Advantages

1. The Slow RSI provides enhanced signal stability by smoothing the RSI calculation, which can help traders better assess market conditions and identify potential overbought or oversold situations.

2. By offering more stable and reliable signals, the Slow RSI may improve the performance of trading strategies based on the RSI, especially in noisy or choppy market conditions.

Disadvantages

1. The smoothing technique employed by the Slow RSI may result in a slower response to changes in price momentum compared to the original RSI. This could lead to delayed signals for entering or exiting trades, which may not be ideal for short-term traders or fast-moving markets.

2. As the Slow RSI is less known and less widely used than the standard RSI, traders may find it more challenging to find resources and support for implementing this variation of the indicator.

The Slow RSI is an interesting modification of the standard RSI, offering potential benefits in terms of signal stability and reliability. However, it is crucial to recognize its limitations, such as a potentially slower response to changes in price momentum. Traders should carefully consider the potential advantages and drawbacks of using the Slow RSI compared to the original RSI before incorporating it into their trading strategies. Ultimately, the choice between the original RSI and the Slow RSI will depend on individual traders' preferences and the specific market conditions they are analyzing.

Ehlers Smoothed RSI

Ehlers Smoothed RSI is a variation of the standard RSI developed by John F. Ehlers, which introduces a smoothing technique to the price input data. The smoothing process involves averaging the current price with the previous two price values, which helps reduce noise and provide a more accurate representation of price momentum. The calculation of up and down price movements remains similar to the original RSI, but the smoothing technique alters the input data.

The primary advantage of Ehlers Smoothed RSI is that it reduces noise and offers a more accurate representation of price momentum, potentially providing more reliable signals for traders.

Comparison with the original RSI

To better understand the potential advantages and disadvantages of Ehlers Smoothed RSI, it is essential to compare its performance against the original RSI.

Advantages

1. Ehlers Smoothed RSI reduces noise by smoothing the price input data, which can help traders better assess market conditions and identify potential overbought or oversold situations.

2. By providing a more accurate representation of price momentum, Ehlers Smoothed RSI may offer more reliable signals for entering or exiting trades, potentially improving the performance of trading strategies based on the RSI.

Disadvantages

1. The smoothing technique employed by Ehlers Smoothed RSI may result in a slower response to changes in price momentum compared to the original RSI. This could lead to delayed signals for entering or exiting trades, which may not be ideal for short-term traders or fast-moving markets.

2. As Ehlers Smoothed RSI is less known and less widely used than the standard RSI, traders may find it more challenging to find resources and support for implementing this variation of the indicator.

Ehlers Smoothed RSI is an intriguing modification of the standard RSI, offering potential benefits in terms of noise reduction and accuracy. However, it is crucial to recognize its limitations, such as a potentially slower response to changes in price momentum. Traders should carefully consider the potential advantages and drawbacks of using Ehlers Smoothed RSI compared to the original RSI before incorporating it into their trading strategies. Ultimately, the choice between the original RSI and Ehlers Smoothed RSI will depend on individual traders' preferences and the specific market conditions they are analyzing.

Cutler's RSI or Rapid RSI

Cutler's RSI is a variation of the standard RSI, which modifies the calculation of average gains and losses. While the original RSI employs exponential moving averages (EMAs) for average gains and losses, Cutler's RSI utilizes simple moving averages (SMAs) instead. This change results in a slightly different behavior of the oscillator compared to the original RSI.

The primary advantage of Cutler's RSI is that it offers a simpler calculation method, which can potentially make it easier to understand and implement for traders. Additionally, by using SMAs, Cutler's RSI may provide a more consistent and stable representation of price momentum.

Comparison with the original RSI

It is essential to recognize the limitations and performance of Cutler's RSI compared to the original RSI to understand its potential advantages and disadvantages better.

Advantages

1. Cutler's RSI has a simpler calculation method, using SMAs instead of EMAs. This makes it easier to understand and implement for traders who prefer a more straightforward approach to technical analysis.

2. By using SMAs, Cutler's RSI may provide a more stable and consistent representation of price momentum, which can help traders better assess market conditions and identify potential overbought or oversold situations.

Disadvantages

1. The use of SMAs in Cutler's RSI may result in a slower response to changes in price momentum compared to the original RSI. This could lead to delayed signals for entering or exiting trades, which may not be ideal for short-term traders or fast-moving markets.

2. As Cutler's RSI is less known and less widely used than the standard RSI, it may be more challenging to find resources and support for implementing this variation of the indicator.

Cutler's RSI is an interesting modification of the standard RSI, offering potential benefits in terms of simplicity and stability. However, it is crucial to recognize its limitations, such as a potentially slower response to changes in price momentum. Traders should carefully consider the potential advantages and drawbacks of using Cutler's RSI compared to the original RSI before incorporating it into their trading strategies. Ultimately, the choice between the original RSI and Cutler's RSI will depend on individual traders' preferences and the specific market conditions they are analyzing.

RSI T3

The T3 RSI is a variation of the standard RSI that introduces the Triple Smoothed Exponential Moving Average (T3) into the calculation process. The primary difference between the T3 RSI and the standard RSI lies in the calculation of the average gains and losses. Instead of using simple moving averages or exponential moving averages, the T3 RSI utilizes T3 to calculate the average gains and losses for up and down price movements.

The primary advantage of the T3 RSI is that it offers enhanced responsiveness and accuracy compared to the original RSI, potentially providing more reliable trading signals for traders.

Comparison with the original RSI

To better understand the potential advantages and disadvantages of the T3 RSI, it is essential to compare its performance against the original RSI.

Advantages

1. The T3 RSI provides enhanced responsiveness and accuracy by incorporating the Triple Smoothed Exponential Moving Average into the calculation of average gains and losses. This can help traders better assess market conditions and identify potential overbought or oversold situations.

2. By offering more responsive and accurate signals, the T3 RSI may improve the performance of trading strategies based on the RSI, especially in fast-moving markets or during periods of high price volatility.

Disadvantages

1. The T3 RSI's increased responsiveness may result in more frequent trading signals, which could lead to higher trading costs or a higher likelihood of false signals.

2. As the T3 RSI is less known and less widely used than the standard RSI, traders may find it more challenging to find resources and support for implementing this variation of the indicator.

The T3 RSI is an innovative modification of the standard RSI, offering potential benefits in terms of responsiveness and accuracy. However, it is crucial to recognize its limitations, such as a potentially higher likelihood of false signals due to increased responsiveness. Traders should carefully consider the potential advantages and drawbacks of using the T3 RSI compared to the original RSI before incorporating it into their trading strategies. Ultimately, the choice between the original RSI and the T3 RSI will depend on individual traders' preferences and the specific market conditions they are analyzing.

RSI DEMA

The DEMA RSI is a variation of the standard RSI that introduces the Double Exponential Moving Average (DEMA) into the calculation process. The primary difference between the DEMA RSI and the standard RSI lies in the calculation of the average gains and losses. Instead of using simple moving averages or exponential moving averages, the DEMA RSI utilizes DEMA to calculate the average gains and losses for up and down price movements.

The primary advantage of the DEMA RSI is that it offers enhanced responsiveness and accuracy compared to the original RSI, potentially providing more reliable trading signals for traders.

Comparison with the original RSI

To better understand the potential advantages and disadvantages of the DEMA RSI, it is essential to compare its performance against the original RSI.

Advantages

1. The DEMA RSI provides enhanced responsiveness and accuracy by incorporating the Double Exponential Moving Average into the calculation of average gains and losses. This can help traders better assess market conditions and identify potential overbought or oversold situations.

2. By offering more responsive and accurate signals, the DEMA RSI may improve the performance of trading strategies based on the RSI, especially in fast-moving markets or during periods of high price volatility.

Disadvantages

1. The DEMA RSI's increased responsiveness may result in more frequent trading signals, which could lead to higher trading costs or a higher likelihood of false signals.

2. As the DEMA RSI is less known and less widely used than the standard RSI, traders may find it more challenging to find resources and support for implementing this variation of the indicator.

The DEMA RSI is an innovative modification of the standard RSI, offering potential benefits in terms of responsiveness and accuracy. However, it is crucial to recognize its limitations, such as a potentially higher likelihood of false signals due to increased responsiveness. Traders should carefully consider the potential advantages and drawbacks of using the DEMA RSI compared to the original RSI before incorporating it into their trading strategies. Ultimately, the choice between the original RSI and the DEMA RSI will depend on individual traders' preferences and the specific market conditions they are analyzing.

Harris' RSI

Harris' RSI is a variation of the standard RSI, designed to address some of its limitations and improve its performance in detecting potential trend reversals and filtering out noise. The key difference between the Harris' RSI and the standard RSI lies in the calculation of average gains and losses. While the standard RSI calculation uses exponential moving averages (EMAs) of gains and losses, Harris' RSI uses a different approach to compute the average gains and losses based on the number of up and down price movements.

The primary advantage of Harris' RSI is that it aims to provide a more adaptive and responsive indicator, making it better suited for detecting potential trend reversals and filtering out noise in the market. By taking into account the number of up and down price movements, Harris' RSI can be more sensitive to changes in the trend, potentially providing earlier signals for entering or exiting trades.

Comparison with the original RSI

While Harris' RSI offers potential improvements over the standard RSI, it is essential to recognize its limitations and compare its performance against the original RSI.

Advantages

1. Harris' RSI can potentially provide earlier signals for trend reversals due to its sensitivity to the number of up and down price movements. This can help traders to identify better entry and exit points in the market.

2. By focusing on the number of up and down price movements, Harris' RSI can filter out noise in the market, reducing the likelihood of false signals that may lead to losing trades.

Disadvantages

1. The increased sensitivity of Harris' RSI to price movements can lead to more frequent signals, which may result in overtrading and increased trading costs.

2. Harris' RSI is less known and less widely used than the standard RSI, which may make it more challenging to find resources and support for implementing this variation of the indicator.

Harris' RSI is an interesting variation of the standard RSI, offering potential advantages in detecting trend reversals and filtering out noise. However, like any technical indicator, it has its limitations and may not be suitable for all trading styles or market conditions. Traders should carefully consider the potential benefits and drawbacks of using Harris' RSI compared to the original RSI before incorporating it into their trading strategies. Ultimately, the choice between the original RSI and Harris' RSI will depend on individual traders' preferences and the specific market conditions they are analyzing.

RSI TEMA

The TEMA RSI is a variation of the standard RSI that introduces the Triple Exponential Moving Average (TEMA) into the calculation process. The primary difference between the TEMA RSI and the standard RSI lies in the calculation of the average gains and losses. Instead of using simple moving averages or exponential moving averages, the TEMA RSI utilizes TEMA to calculate the average gains and losses for up and down price movements.

The primary advantage of the TEMA RSI is that it offers enhanced responsiveness and accuracy compared to the original RSI, potentially providing more reliable trading signals for traders.

Comparison with the original RSI

To better understand the potential advantages and disadvantages of the TEMA RSI, it is essential to compare its performance against the original RSI.

Advantages

1. The TEMA RSI provides enhanced responsiveness and accuracy by incorporating the Triple Exponential Moving Average into the calculation of average gains and losses. This can help traders better assess market conditions and identify potential overbought or oversold situations.

2. By offering more responsive and accurate signals, the TEMA RSI may improve the performance of trading strategies based on the RSI, especially in fast-moving markets or during periods of high price volatility.

Disadvantages

1. The TEMA RSI's increased responsiveness may result in more frequent trading signals, which could lead to higher trading costs or a higher likelihood of false signals.

2. As the TEMA RSI is less known and less widely used than the standard RSI, traders may find it more challenging to find resources and support for implementing this variation of the indicator.

The TEMA RSI is an innovative modification of the standard RSI, offering potential benefits in terms of responsiveness and accuracy. However, it is crucial to recognize its limitations, such as a potentially higher likelihood of false signals due to increased responsiveness. Traders should carefully consider the potential advantages and drawbacks of using the TEMA RSI compared to the original RSI before incorporating it into their trading strategies. Ultimately, the choice between the original RSI and the TEMA RSI will depend on individual traders' preferences and the specific market conditions they are analyzing.

Jurik RSX

The Jurik RSX, developed by Mark Jurik, is a variation of the standard RSI that aims to provide a smoother and more responsive indicator by applying a unique smoothing algorithm based on a series of recursive calculations. The Jurik RSX calculates the price momentum (mom) and the absolute price momentum (moa) using a three-stage filtering process, which ultimately results in a smoother and more responsive output compared to the original RSI.

Comparison with the original RSI

To better understand the potential benefits and drawbacks of the Jurik RSX, it is essential to compare its performance against the original RSI.

Advantages

1. The Jurik RSX offers enhanced responsiveness and smoothness due to its unique recursive filtering process, allowing traders to better identify potential trend reversals, overbought, and oversold conditions.

2. The improved responsiveness of the Jurik RSX may result in more timely trading signals, helping traders to capitalize on opportunities more effectively, especially in fast-moving markets or during periods of high price volatility.

Disadvantages

1. The increased complexity of the Jurik RSX calculation may make it more challenging for traders to understand and implement compared to the original RSI.

2. As the Jurik RSX is less known and less widely used than the standard RSI, traders may find it more difficult to find resources and support for implementing this variation of the indicator.

The Jurik RSX is an innovative modification of the standard RSI, offering potential benefits in terms of responsiveness and smoothness. However, it is crucial to recognize its limitations, such as increased complexity and limited resources compared to the original RSI. Traders should carefully consider the potential advantages and drawbacks of using the Jurik RSX before incorporating it into their trading strategies. Ultimately, the choice between the original RSI and the Jurik RSX will depend on individual traders' preferences and the specific market conditions they are analyzing.

Additional Features

This indicator allows you to select from 33 source types. They are as follows:

Close

Open

High

Low

Median

Typical

Weighted

Average

Average Median Body

Trend Biased

Trend Biased (Extreme)

HA Close

HA Open

HA High

HA Low

HA Median

HA Typical

HA Weighted

HA Average

HA Average Median Body

HA Trend Biased

HA Trend Biased (Extreme)

HAB Close

HAB Open

HAB High

HAB Low

HAB Median

HAB Typical

HAB Weighted

HAB Average

HAB Average Median Body

HAB Trend Biased

HAB Trend Biased (Extreme)

What are Heiken Ashi "better" candles?

Heiken Ashi "better" candles are a modified version of the standard Heiken Ashi candles, which are a popular charting technique used in technical analysis. Heiken Ashi candles help traders identify trends and potential reversal points by smoothing out price data and reducing market noise. The "better formula" was proposed by Sebastian Schmidt in an article published by BNP Paribas in Warrants & Zertifikate, a German magazine, in August 2004. The aim of this formula is to further improve the smoothing of the Heiken Ashi chart and enhance its effectiveness in identifying trends and reversals.

Standard Heiken Ashi candles are calculated using the following formulas:

Heiken Ashi Close = (Open + High + Low + Close) / 4

Heiken Ashi Open = (Previous Heiken Ashi Open + Previous Heiken Ashi Close) / 2

Heiken Ashi High = Max (High, Heiken Ashi Open, Heiken Ashi Close)

Heiken Ashi Low = Min (Low, Heiken Ashi Open, Heiken Ashi Close)

The "better formula" modifies the standard Heiken Ashi calculation by incorporating additional smoothing, which can help reduce noise and make it easier to identify trends and reversals. The modified formulas for Heiken Ashi "better" candles are as follows:

Better Heiken Ashi Close = (Open + High + Low + Close) / 4

Better Heiken Ashi Open = (Previous Better Heiken Ashi Open + Previous Better Heiken Ashi Close) / 2

Better Heiken Ashi High = Max (High, Better Heiken Ashi Open, Better Heiken Ashi Close)

Better Heiken Ashi Low = Min (Low, Better Heiken Ashi Open, Better Heiken Ashi Close)

Smoothing Factor = 2 / (N + 1), where N is the chosen period for smoothing

Smoothed Better Heiken Ashi Open = (Better Heiken Ashi Open * Smoothing Factor) + (Previous Smoothed Better Heiken Ashi Open * (1 - Smoothing Factor))

Smoothed Better Heiken Ashi Close = (Better Heiken Ashi Close * Smoothing Factor) + (Previous Smoothed Better Heiken Ashi Close * (1 - Smoothing Factor))

The smoothed Better Heiken Ashi Open and Close values are then used to calculate the smoothed Better Heiken Ashi High and Low values, resulting in "better" candles that provide a clearer representation of the market trend and potential reversal points.

It's important to note that, like any other technical analysis tool, Heiken Ashi "better" candles are not foolproof and should be used in conjunction with other indicators and analysis techniques to make well-informed trading decisions.

Heiken Ashi "better" candles, as mentioned previously, provide a clearer representation of market trends and potential reversal points by reducing noise and smoothing out price data. When using these candles in conjunction with other technical analysis tools and indicators, traders can gain valuable insights into market behavior and make more informed decisions.

To effectively use Heiken Ashi "better" candles in your trading strategy, consider the following tips:

Trend Identification: Heiken Ashi "better" candles can help you identify the prevailing trend in the market. When the majority of the candles are green (or another color, depending on your chart settings) and there are no or few lower wicks, it may indicate a strong uptrend. Conversely, when the majority of the candles are red (or another color) and there are no or few upper wicks, it may signal a strong downtrend.

Trend Reversals: Look for potential trend reversals when a change in the color of the candles occurs, especially when accompanied by longer wicks. For example, if a green candle with a long lower wick is followed by a red candle, it could indicate a bearish reversal. Similarly, a red candle with a long upper wick followed by a green candle may suggest a bullish reversal.

Support and Resistance: You can use Heiken Ashi "better" candles to identify potential support and resistance levels. When the candles are consistently moving in one direction and then suddenly change color with longer wicks, it could indicate the presence of a support or resistance level.

Stop-Loss and Take-Profit: Using Heiken Ashi "better" candles can help you manage risk by determining optimal stop-loss and take-profit levels. For instance, you can place your stop-loss below the low of the most recent green candle in an uptrend or above the high of the most recent red candle in a downtrend.

Confirming Signals: Heiken Ashi "better" candles should be used in conjunction with other technical indicators, such as moving averages, oscillators, or chart patterns, to confirm signals and improve the accuracy of your analysis.

In this implementation, you have the choice of AMA, KAMA, or T3 smoothing. These are as follows:

Kaufman Adaptive Moving Average (KAMA)

The Kaufman Adaptive Moving Average (KAMA) is a type of adaptive moving average used in technical analysis to smooth out price fluctuations and identify trends. The KAMA adjusts its smoothing factor based on the market's volatility, making it more responsive in volatile markets and smoother in calm markets. The KAMA is calculated using three different efficiency ratios that determine the appropriate smoothing factor for the current market conditions. These ratios are based on the noise level of the market, the speed at which the market is moving, and the length of the moving average. The KAMA is a popular choice among traders who prefer to use adaptive indicators to identify trends and potential reversals.

Adaptive Moving Average

The Adaptive Moving Average (AMA) is a type of moving average that adjusts its sensitivity to price movements based on market conditions. It uses a ratio between the current price and the highest and lowest prices over a certain lookback period to determine its level of smoothing. The AMA can help reduce lag and increase responsiveness to changes in trend direction, making it useful for traders who want to follow trends while avoiding false signals. The AMA is calculated by multiplying a smoothing constant with the difference between the current price and the previous AMA value, then adding the result to the previous AMA value.

T3

The T3 moving average is a type of technical indicator used in financial analysis to identify trends in price movements. It is similar to the Exponential Moving Average (EMA) and the Double Exponential Moving Average (DEMA), but uses a different smoothing algorithm.

The T3 moving average is calculated using a series of exponential moving averages that are designed to filter out noise and smooth the data. The resulting smoothed data is then weighted with a non-linear function to produce a final output that is more responsive to changes in trend direction.

The T3 moving average can be customized by adjusting the length of the moving average, as well as the weighting function used to smooth the data. It is commonly used in conjunction with other technical indicators as part of a larger trading strategy.

█ Giga Kaleidoscope Modularized Trading System

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?